Enabling Insurance agents to seamlessly manage their insurance process.

Lami is an end-to-end digital insurance platform enabling insurance agents and brokers to digitize their insurance processes. Lami enables insurance agents to onboard new customers in one integrated platform.

Read more

More Insurance Solutions for Agents

Insurance agents

Sell any type of insurance and get your commission paid instantly

Use our powerful app to access insurance products the Seamless way.

Sell a wide range of insurance products to meet the diverse needs of your clients, including auto, health, life, and more. Easily manage and track your sales with our intuitive app, designed to make selling insurance a seamless and efficient experience.

Become an agent

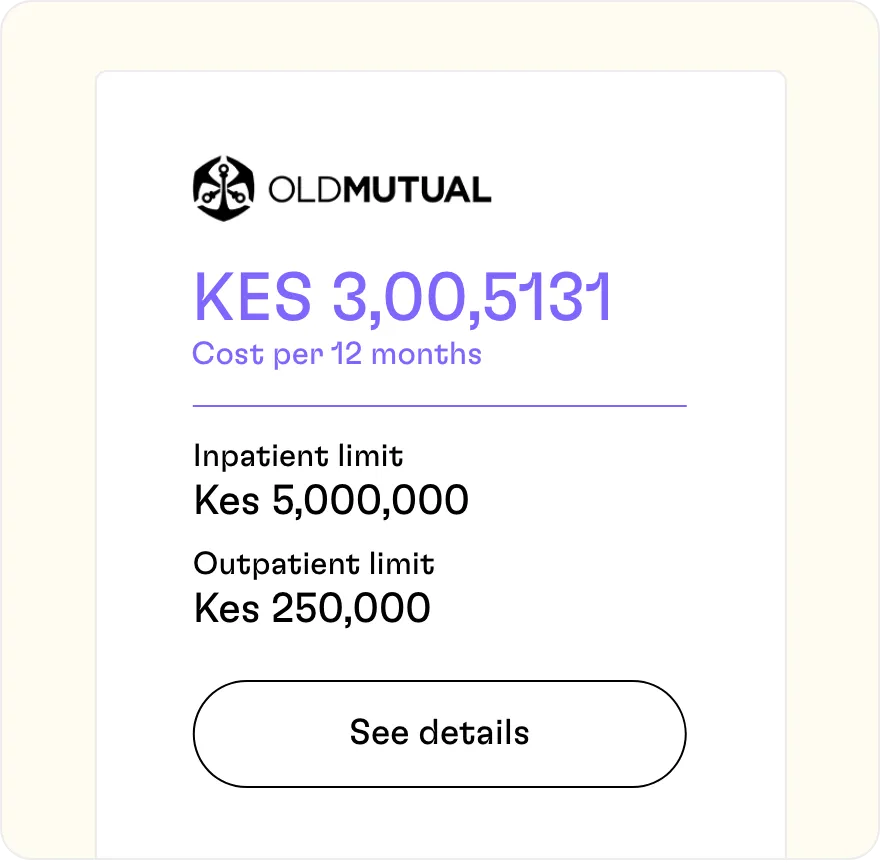

Plans that fit your customer’s needs, All Backed by Major Underwriters

Our platform empowers agents to effortlessly compare multiple quotes from leading underwriters, ensuring you get the best deal for your customers. With just a few clicks, explore a wide range of insurance options tailored to your clients' specific requirements.

Become an agent

Easily process renewals, and track your insurance claims in real-time.

With our user-friendly interface, agents can effortlessly manage payments, renewals, and claims, all while monitoring live quotes to stay ahead of the competition and meet their clients' evolving requirements.

Become an agent

Why Choose Lami.

Enjoy the convenience of getting your commissions paid out daily after each sale, allowing you to focus on growing your business.

Receive your commissions payments daily.

Receive your commissions payments daily.

Guaranteed Best price in the market.

Guaranteed Best price in the market.

30+ insurance companies on our platform.

30+ insurance companies on our platform.

Easy and seamless platform.

Easy and seamless platform.

Small businesses

Easily budget for employee medical plans without compromising on cover.

Get a quote for the essential insurance products your business needs.

Choose pricing that suits your budget and compare cover options.

Use dynamic filters to find the right product from all the major underwriters.

Review multiple plans, pricing, and cover before you commit.

What Agents Using Lami Say

Stephen Monari

Discover how Lami's seamless insurance solutions allow Steven to offer immediate coverage to his customers, saving time and enhancing the buying experience.

Moses Njuguna

"It's incredible that I can provide my customers with insurance immediately after they purchase a car from me," shares the director of AutoCad Motors Runda

Gadson Njoroge

Lami is more than just a platform, it exemplifies our ongoing support for insurance agents, helping them simplify the insurance process and grow their business.

Regine Aswa

Listen to our esteemed insurance agents as they share their thoughts on our platform since we began the journey. Lami is always seeking feedback to help us improve the experience